Generate income by selling insurance on the market at attractive prices with edge. Defined max loss. Positive convexity. Optimized daily.

Watch Video Explainer

How Does it Work?

Every day, Helium looks through the universe of all possible options credit ratio spreads to find trades that best satisfy a balanced combination of:

1.) High Market Expected Value (expected value): Helium tries to maximize the expected terminal value of each position, as determined by market prices & Black-Scholes implied probabilities. Helium uses conservative assumptions to reduce the likelihood of false positives.

2.) High Helium Expected Value (expected value): Using highly regularized machine learning on historical options prices, Helium tries to maximize the expected terminal value of each trade.

3.) High Theta (theta): This represents the daily time decay of options, or the daily “carry” received for selling options.

4.) Small Vega (vega): Helium tries to minimize the sensitivity of sold options to changes in implied volatility in order to reduce risk to increases in uncertainty & underlying movement.

5.) Helium Uncertainty < Market Uncertainty: By comparing market uncertainty to Helium uncertainty, we can seek out underlyings with potentially over-priced risk.

6.) Large Credit Received: Looking for options premium to generate profits means trying to maximize the options premium received.

7.) Short Trade Duration: Helium optimizes for options close to expiration in order to maximize the annualized percent return.

8.) High Maximum Option Lifetime Value: Helium trains an AI to predict maximum price over an options lifetime. Then, it optimizes to maximize this value for the long leg of the option and minimize this value for the short leg.

9.) High Probability of Profit: Helium is looking to sell options that have a high probability of expiring worthless (so we can keep the whole credit received when we sold it).

10.) Defined Risk: All Helium trades have a maximum defined risk going into each trade by finding a cost-efficient hedge and trying to minimize the max potential loss.

11.) AI Price Forecasts: Using meta machine learning price forecasts, Helium weights short put options higher on bullish stocks (long delta) and weighs short call options higher on bearish stocks (short delta).

12.) High Implied Volatility Rank: (IVR) Helium is looking for assets with higher IV relative to yearly highs and lows in order to take advantage of IV compression of relatively more expensive options.

13.) High Liquidity: Helium optimizes for trades with tighter markets as measured by the bid-ask spread.

14.) High Historical Performance: Helium optimizes for models with a historically high risk-adjusted return if you had opened up a new trade every day it was available.

15.) Selling High IV & Buying Low IV: On a relative basis, Helium optimizes for selling options with higher implied volatility and buying options with relatively low implied volatility.

One Click Trade Execution: Automatic limit order algorithm to get filled at attractive prices

Trading Helium’s Short Volatility

To find the daily-updated trades, click the red “Short Volatility” buttons on Short Volatility Forecasts.

These trades are updated daily on potentially attractive market prices, predominantly reward:risk and expected value.

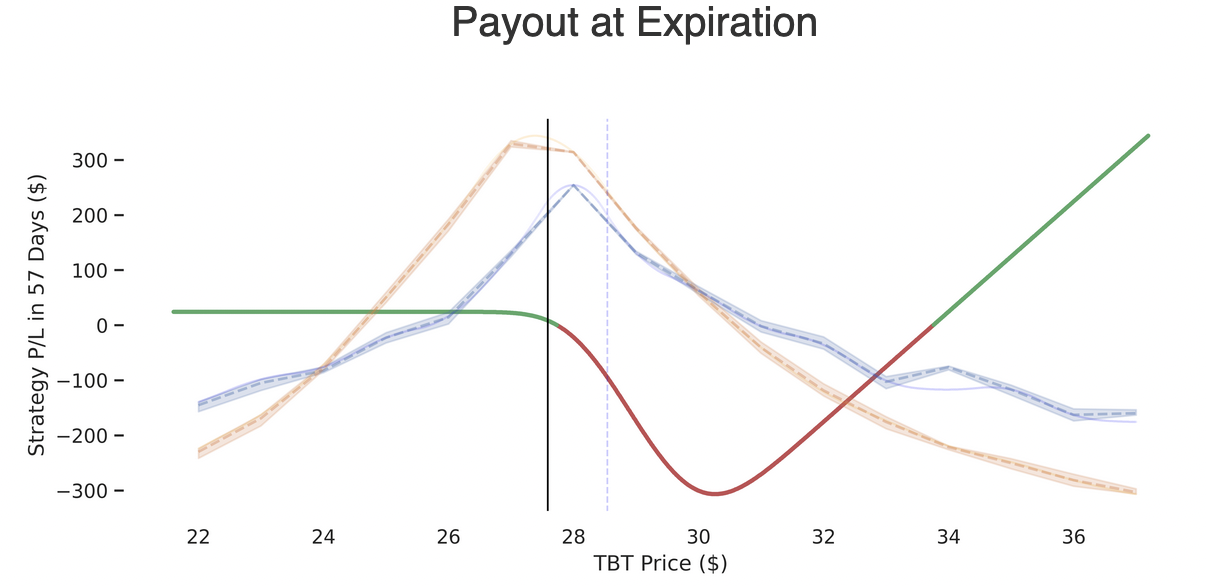

Example Trade & Risk Profile

Most of Helium’s Short Volatility trades are ratio spreads, which means selling 1 expensive option and buying 2 cheaper options to hedge.

In the below example, we are selling a call option struck at $27 and buying 2 call options struck at $30

Trade Metrics

Delta Risk

Risk from underlying movement. In this example, you can see that this trade will be profitable if the price in 7 days is below $28 or above $34.

Vega Risk

Risk from increases in uncertainty, or increases in implied volatility right now. In this example, you can see that we are initially short volatility.

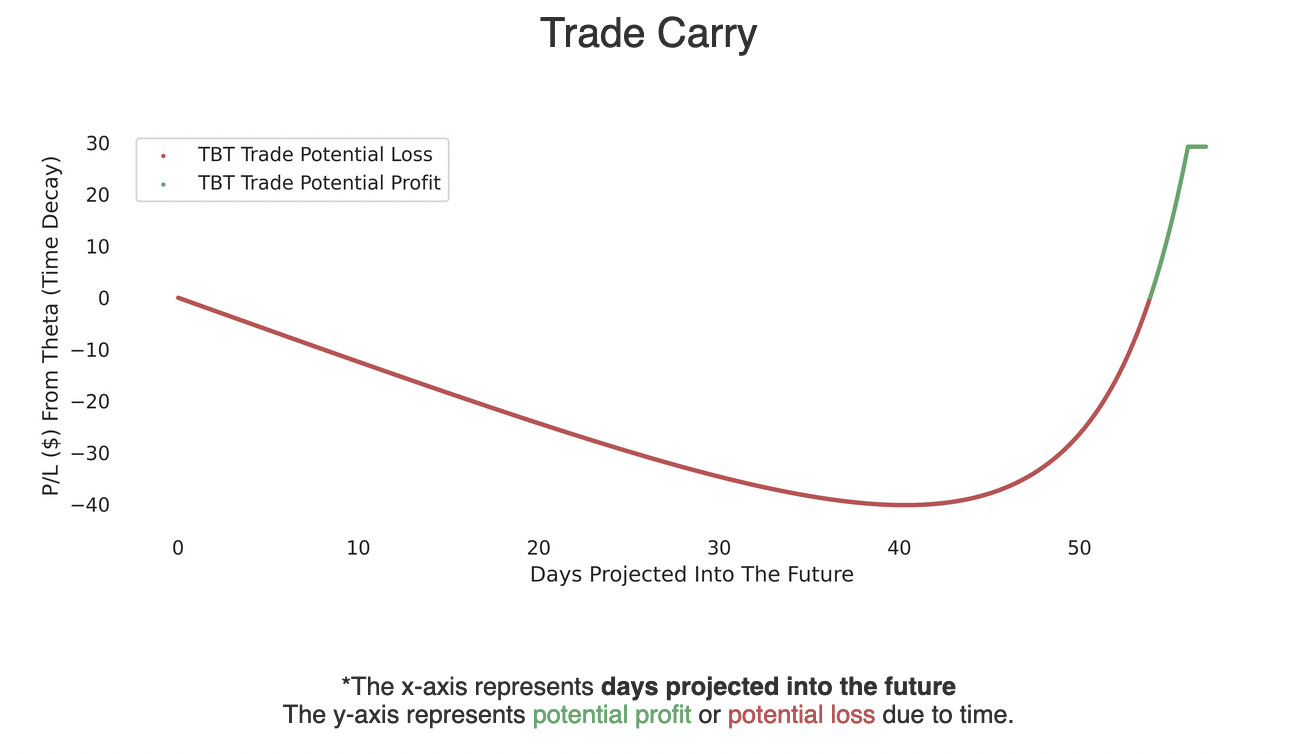

Theta Risk

Risk from time decay if nothing else happens right now. In this example, you can see we are initially short carry, but could become long carry over time.

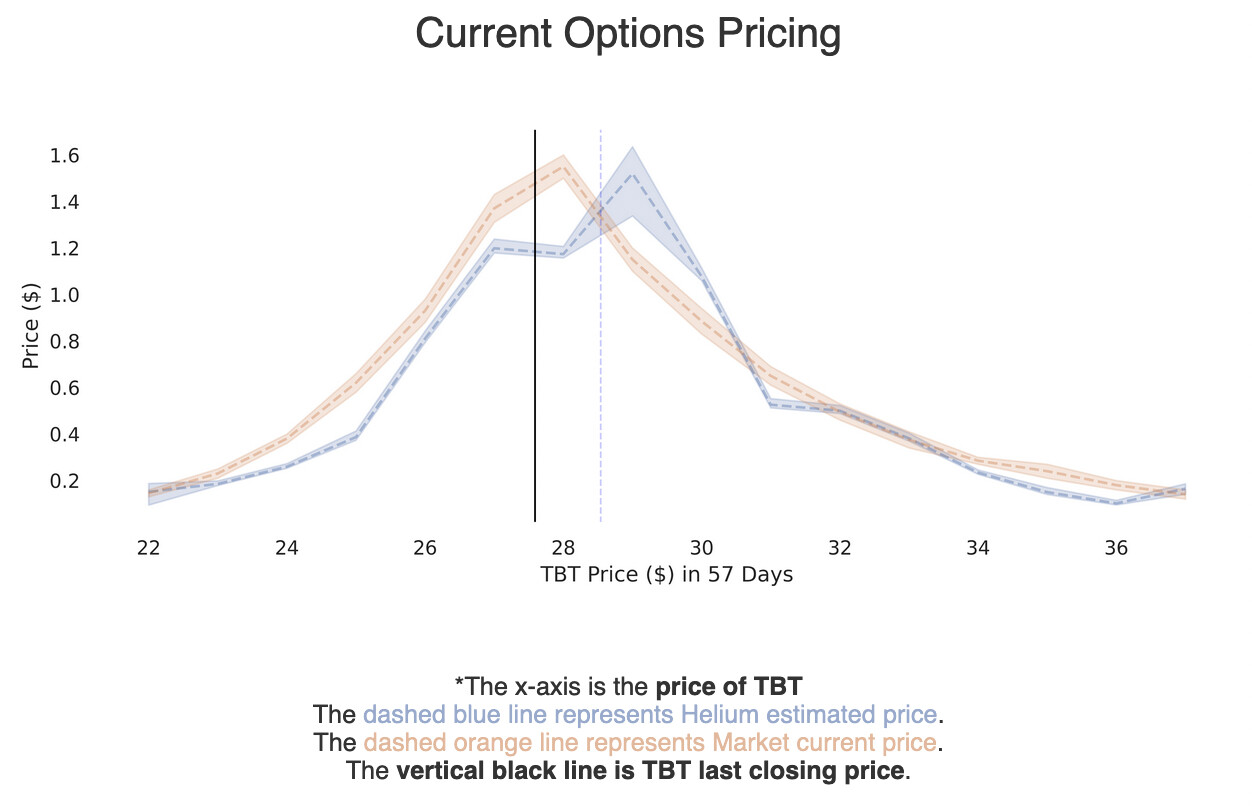

Current Options Pricing

Market vs Helium AI options prices. In this example, you can see that Helium thinks the $27 strike is overprices (the option we are selling) and the $30 strike is underpriced (the options we are buying).

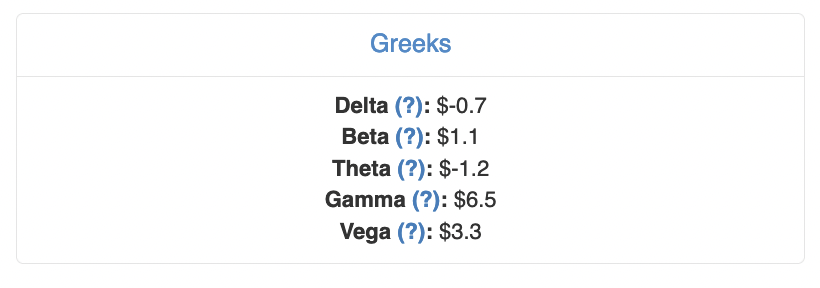

Greek Risks

Current greek risk metrics, where Beta is delta-weighted to SPY. These are numerical ways of looking at the above graphs.

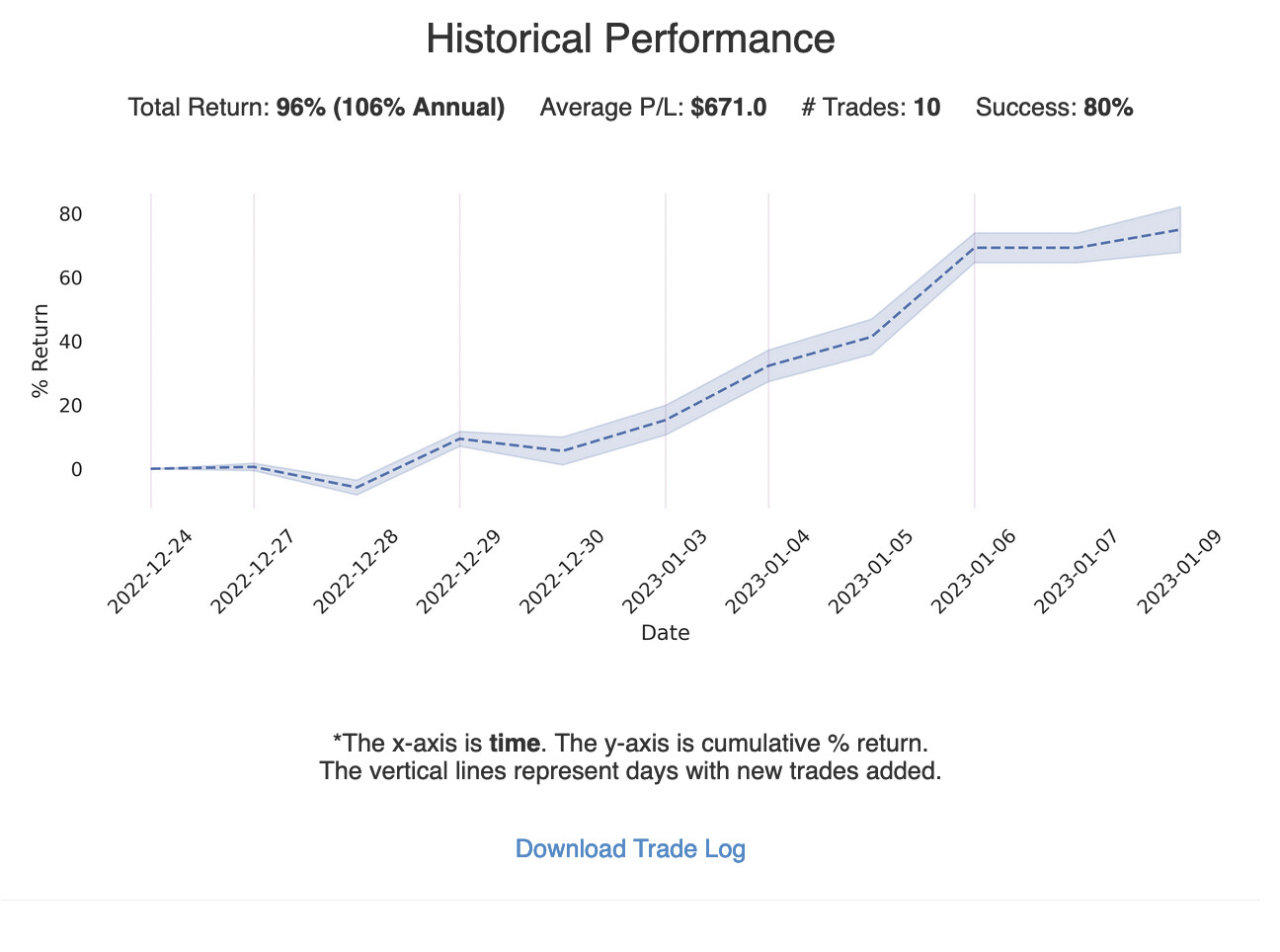

Historical Performance

Cumulative return if you had opened a Short Volatility trade every day.

See Also: Long Volatility: Using Helium to Buy Options

*Disclaimer: Nothing on Helium Trades or our blog constitutes investment advice, performance data or any recommendation that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. Helium Trades is not responsible in any way for the accuracy of any model predictions, price data, or trading.Any mention of a particular security and related prediction data is not a recommendation to buy or sell that security. Investments in securities involve the risk of loss. Past performance is no guarantee of future results. Helium Trades is not responsible for any of your investment decisions. You should consult a financial expert before engaging in any transaction.